India Climbs to 3rd place Globally as Tech Startup Ecosystem Raises $7.7B in 9M 2025

Bengaluru, 25 September 2025: Tracxn, a leading market intelligence platform, has released its latest India Tech Funding 9M 2025 report. The proprietary report provides key insights into India’s technology ecosystem, highlighting funding raised by startups, major industry players, and the key trends shaping the sector’s landscape.

In 9M 2025, India’s tech startups raised $7.7B, marking a 23% decline compared to $10.1B in 9M 2024 and a 6% drop from $8.3B in 9M 2023. During this period, India ranked as the third-highest funded country globally, ahead of Germany and France, and behind only the US and UK.

Funding trends varied across stages. Seed Stage funding witnessed a total of $727M, a 39% decline compared to $1.2B in 9M 2024, and a 34% drop from $1.1B in 9M 2023. Early Stage funding totaled $2.7B, down 10% from $3.0B in 9M 2024, but on par with 9M 2023 levels. Late Stage funding raised a total funding of $4.3B, marking a 27% decline from $5.9B in 9M 2024, and a 4% drop compared to $4.5B raised in 9M 2023.

Commenting on the findings, Neha Singh, Co-Founder of Tracxn, said, “India climbing to the 3rd rank globally reflects the resilience and adaptability of our startup ecosystem. What we are witnessing is a clear shift toward maturity, with rising acquisitions, steady IPO activity, and continued unicorn creation providing balanced exit pathways for founders and investors. At the same time, sectors such as Enterprise Applications, Retail, and Transportation & Logistics Tech are driving long-term investor confidence and fueling India’s digital transformation. This combination of resilience in funding, momentum in exits, and strength across core sectors reinforces India’s standing as one of the most dynamic and globally competitive technology hubs.”

9M 2025 witnessed 10 $100M+ funding rounds, compared to 16 in 9M 2024 and 15 in 9M 2023. Notable rounds included Erisha E Mobility ($1B, Series D), GreenLine ($275M, Series A), Infra.Market ($222M, Series F). Some of the others included Access Healthcare and Groww. The median round size doubled to $1.5M from $683K in 9M 2024.

The report highlights that Enterprise Applications, Retail, and Transportation & Logistics Tech were the top-performing sectors in 9M 2025. Enterprise Applications received $2.3B, which was a 6% decrease compared to $2.5B raised in 9M 2024, but a 2% increase compared to $2.2B raised in 9M 2023. Retail received $2.0B in funding, marking an 18% decline compared to $2.4B raised in 9M 2024, but a 15% rise compared to $1.7B raised in 9M 2023. Transportation & Logistics Tech received $1.79B, reflecting a 17% increase compared to $1.53B raised in 9M 2024, and a 2% drop compared to $1.82B raised in 9M 2023.

In terms of exits, 110 acquisitions took place during 9M 2025, a 15% increase over 96 in 9M 2024 and a drop of 5% compared to 116 acquisitions in 9M 2023. The largest deal was Resulticks’ $2.0B acquisition by Diginex. This became the highest valued acquisition in 9M 2025, followed by Magma General Insurance’s $516M acquisition by DS Group and Patanjali Ayurved. Enterprise Applications continued to lead acquisition activity during this period, driven by demand for cloud and AI solutions. Bengaluru topped city-level acquisition activity with 35 deals, followed by Mumbai (19), Gurugram (11), and Delhi (9), highlighting the ongoing dominance of Tier 1 hubs. On the investor side, Peak XV Partners and Elevation Capital were among the most prominent, leading exits with 14 and 8 rounds, respectively.

IPO activity remained strong, with 26 companies going public in 9M 2025. Urban, DevX, BlueStone, and iCodex were among the notable listings. Real Estate & Construction Tech and Enterprise Applications dominated IPO activity with six listings each during this period, marking a shift in market readiness, while Energy Tech also gained momentum with five listings, reflecting rising demand for clean energy solutions. Investors like Accel (12 rounds), Hero MotoCorp (8 rounds), and Saama Capital (8 rounds) actively exited via IPOs, capitalizing on higher valuations while enabling companies to access fresh growth capital and scale further.

There were 4 unicorns created in 9M 2025, compared to 5 in 9M 2024 and 1 in 9M 2023. India is now home to 122 unicorns, of which 22 have already exited through IPOs or acquisitions - signaling increasing maturity and depth in the ecosystem. Bengaluru continues to dominate India’s unicorn landscape, hosting 53 unicorns, followed by Gurugram (20) and Mumbai (18). Retail ($34.9B) and Enterprise Applications ($18.9B) have emerged as the leading sectors by cumulative equity funding raised by unicorns. On profitability, Zerodha stood out as the most successful unicorn, with $1.2B in revenue and $663M in profit in FY 2023–24.

Bengaluru-based startups continued to dominate, accounting for 31% of total funding, followed by Delhi at 18%. LetsVenture, AngelList and Accel emerged as the top all-time investors. Inflection Point Ventures, Venture Catalysts, and Antler were the top seed-stage investors; Peak XV Partners, Vertex Ventures, and Accel led early-stage investments; while Premji Invest, Sofina, and SoftBank Vision Fund were the top late-stage investors.

Popular Categories

Read More Articles

Business

Five Electric Scooters You Can Buy for Less Than the Price of the iPhone 17 Pro Max by Awadh 360° Desk September 19, 2025

Travel and Tourism

One ‘Incredible India’ campaign isn't enough: Shashi Tharoor on rebranding tourism by Awadh 360° Desk September 18, 2025

Business

Misfits - India's first Prebiotic soda brand raises an undisclosed funding by Awadh 360° Desk September 8, 2025

Travel and Tourism

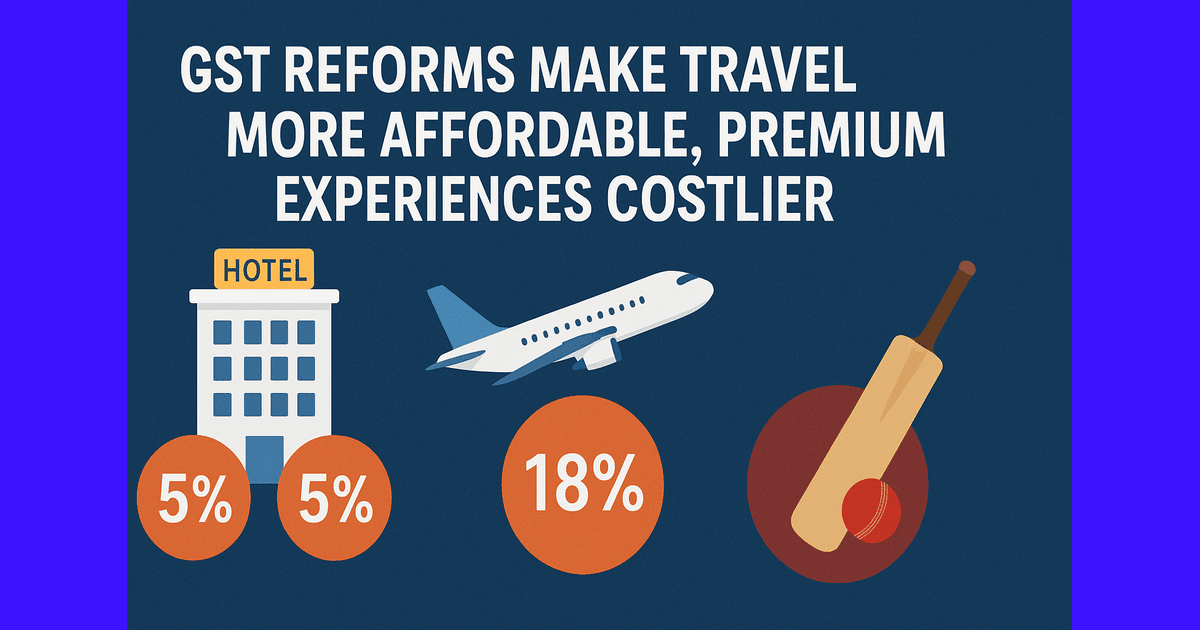

GST Reforms Make Travel More Affordable, Premium Experiences Costlier by Awadh 360° Desk September 5, 2025